New L4M1 Test Tutorial - L4M1 Valid Exam Sims

Wiki Article

BONUS!!! Download part of DumpsFree L4M1 dumps for free: https://drive.google.com/open?id=1yJDlB9sje6TAVMiDNezhIrjTqSv8F0tO

The downloading process is operational. It means you can obtain L4M1 quiz torrent within 10 minutes if you make up your mind. Do not be edgy about the exam anymore, because those are latest L4M1 exam torrent with efficiency and accuracy. You will not need to struggle with the exam. Besides, there is no difficult sophistication about the procedures, our latest L4M1 Exam Torrent materials have been in preference to other practice materials and can be obtained immediately.

CIPS L4M1 Exam copyright Topics:

| Topic | Details |

|---|---|

| Topic 1 |

|

| Topic 2 |

|

| Topic 3 |

|

New New L4M1 Test Tutorial 100% Pass | Efficient L4M1 Valid Exam Sims: Scope and Influence of Procurement and Supply

It is inescapable choice to make why don't you choose our L4M1 practice materials with passing rate up to 98-100 percent. You can have a sweeping through of our L4M1 practice materials with intelligibly and under-stable contents. It is time to take the plunge and you will not feel depressed. All incomprehensible issues will be small problems and all contents will be printed on your minds. So even trifling mistakes can be solved by using our L4M1 practice materials, as well as all careless mistakes you may make.

CIPS Scope and Influence of Procurement and Supply Sample Questions (Q20-Q25):

NEW QUESTION # 20

Bob is a procurement manager at ABC Ltd. He has been asked to ensure all future purchases achieve 'value for money' for the organisation. What is meant by 'value for money'? (5 points). Describe 4 techniques that Bob could use to achieve this (20 points)

Answer:

Explanation:

See the solution in Explanation part below

Explanation:

1) A definition of Value for Money: ensuring a purchase is cost effective. This may be that the purchase achieves the 5 Rights of Procurement or that the purchase achieves the 4Es: Economy, Efficiency, Effectiveness and Equity. - this is only worth 5 points, so don't spend too long on this

2) 4 techniques Bob can use to achieve VFM: this is the bulk of your essay. Each of the 4 will be worth 5 points, so remember to give a thorough and example. Pick 4 from the list below: complete a value analysis to eliminate non-essential features, minimise variety/ consolidate demand, avoid over specification, pro-active sourcing, whole life costing methodologies, eliminate / reduce inventory, use electronic systems, international sourcing, sustainability / environmental policies, currency/ exchange rate considerations, negotiating good payment terms, packaging, warrantees.

Example Essay:

"Value for money" (VFM) is a concept that refers to obtaining the best possible return on investment or benefits relative to the cost incurred. It involves assessing whether the goods, services, or activities provided offer an optimal balance between their cost and the quality, benefits, or outcomes they deliver. Value for money is not solely about choosing the cheapest option; instead, it considers the overall efficiency, effectiveness, and long-term value derived from an expenditure. For Bob, the Procurement Manager at ABC Ltd there are four key ways that he can achieve this for all future purchases.

Value Engineering

This is looking at the components of a product and evaluating the value of each component individually. You can then eliminate any components that do not add value to the end product. To do this Bob would choose a product to review and determine whether any parts of this can be omitted (thus saving the company money) or could be replaced by components that are of a higher quality at the same price (thus providing added value to the customer). For example, Bob could complete a Value Engineering exercise on the new mobile phone prototype ABC plan to release next year. His findings may discover a way to provide a higher quality camera at no additional cost or that some components don't add value and can be eliminated.

Consolidate demand

Bob can achieve value for money by consolidating demand at ABC ltd. This would mean rather than each individual person/ department ordering what they want when they need it, Bob creates a centralised process for ordering items in bulk for the departments to share. For example, if each department require stationary to be ordered, Bob can consolidate this demand and create one big order each quarter. This will likely result in cost savings for ABC as suppliers often offer discounts for large orders. Moreover, consolidating demand will allow for saving in time (one person does the task once, rather than lots of people doing the same task and duplicating work).

International sourcing

Bob may find there is value for money in changing suppliers and looking at international sourcing. Often other countries outside of the UK can offer the same products at a lower cost. An example of this is manufactured goods from Chin a. By looking at international supply chains, Bob may be able to make cost-savings for ABC. He should be sure that when using this technique there is no compromise on quality.

Whole Life Costing methodology

This is a technique Bob can use for procuring capital expenditure items for ABC. This involves looking at the costs of the item throughout its lifecycle and not just the initial purchase price. For example, if Bob needs to buy a new delivery truck he should consider not only the price of the truck, but also the costs of insurance for the truck, how expensive it is to buy replacement parts such as tyres and the cost of disposing of the truck once it reaches the end of its life. By considering these factors Bob will ensure that he buys the truck that represents the best value for money long term.

In conclusion Bob should ensure he uses these four techniques for all items he and his team procures in the future. This will ensure ABC Ltd are always achieving value for money, and thus remain competitive in the marketplace.

Tutor Notes

- This case study is really short, and the ones you'll receive in the exam are often longer and give you more guidance on what they're expecting you to write. With case study questions, you have to make your entire answer about Bob. So don't bring in examples from your own experience, rather, focus on giving examples for Bob.

- A good rule of thumb for case study questions is make sure you reference the case study once per paragraph.

- Value for Money is a really broad topic and you can pretty much argue anything that procurement does is helping to achieve value for money. There's a large table of stuff that's considered VFM on p.38 but that table isn't exhaustive. So feel free to come up with your own ideas for this type of essay.

Some additional tidbits of information on VFM:

- The 'academic' definition of Value for Money is 'the optimum combination of whole life cost and the quality necessary to meet the customer's requirement'

- Value for Money is an important strategic objective for most organisations but particularly in the public sector. This is because the public sector is financed by public money (taxes), so they must demonstrate that the organisation is using this money wisely. This might be an interesting fact to put into an essay on VFM.

- Value can often be hard to quantify, particularly in the service industry. E.g. in customer service it can be difficult to quantify the value of having knowledgeable and polite employees delivering the service.

NEW QUESTION # 21

Provide a definition of a stakeholder (5 points) and describe 3 categories of stakeholders (20 points).

Answer:

Explanation:

See the solution in Explanation part below

Explanation:

Essay Plan:

Definition of Stakeholder- someone who has a 'stake' or interest in the company. A person or organisation who influences and can be influenced by the company.

Categories of stakeholders:

1) Internal Stakeholders- these people work inside the company e.g. employees, managers etc

2) Connected- these people work with the company e.g. suppliers, mortgage lenders

3) External Stakeholders - these people are outside of the company e.g. the government, professional bodies, the local community.

Example Essay:

A stakeholder is an individual, group, or entity that has a vested interest or concern in the activities, decisions, or outcomes of an organization or project. Stakeholders are those who can be affected by or can affect the organization, and they play a crucial role in influencing its success, sustainability, and reputation. Understanding and managing stakeholder relationships is a fundamental aspect of effective organizational governance and decision-making and there are several different types of stakeholders.

Firstly, internal stakeholders are those individuals or groups directly connected to the daily operations and management of the organization. Internal stakeholders are key to success and are arguably more vested in the company succeeding. They may depend on the company for their income / livelihood. Anyone who contributes to the company's internal functions can be considered an internal stakeholder for example:

This category includes

1) Employees: With a direct influence on the organization's success, employees are critical internal stakeholders. Their engagement, satisfaction, and productivity impact the overall performance.

2) Management and Executives: The leadership team has a significant influence on the organization's strategic direction and decision-making. Their decisions can shape the company's future.

Secondly, connected stakeholders are those individuals or groups whose interests are tied to the organization but may not be directly involved in its day-to-day operations. Connected stakeholders work alongside the organisation and often have a contractual relationship with the organisation. For example, banks, mortgage lenders, and suppliers. These stakeholders have an interest in the business succeeding, but not as much as internal stakeholders. It is important to keep these stakeholders satisfied as the organisation does depend on them to some extent. For example, it is important that the organisation has a good relationship with their bank / mortgage provider/ supplier as failing to pay what they owe may result in the stakeholders taking legal action against the organisation.

This category includes:

1) Shareholders/Investors: Holding financial stakes in the organization, shareholders seek a return on their investment and have a vested interest in the company's financial performance.

2) Suppliers and Partners: External entities providing goods, services, or collaboration. Their relationship with the organization impacts the quality and efficiency of its operations.

Lastly external stakeholders are entities outside the organization that can influence or be influenced by its actions. This category includes anyone who is affected by the company but who does not contribute to internal operations. They have less power to influence decisions than internal and connected stakeholders. External stakeholders include the government, professional bodies, pressure groups and the local community. They have quite diverse objectives and have varying ability to influence the organisation. For example, the government may be able to influence the organisation by passing legislation that regulates the industry but they do not have the power to get involved in the day-to-day affairs of the company. Pressure groups may have varying degrees of success in influencing the organisation depending on the subject matter. This category includes:

1) Customers: With a direct impact on the organization's revenue, customers are vital external stakeholders. Their satisfaction and loyalty are crucial for the company's success.

2) Government and Regulatory Bodies: External entities overseeing industry regulations. Compliance with these regulations is crucial for the organization's reputation and legal standing.

In conclusion, stakeholders are diverse entities with a vested interest in an organization's activities. The three categories-internal, connected and external -encompass various groups that significantly influence and are influenced by the organization. Recognizing and addressing the needs and concerns of stakeholders are vital for sustainable and responsible business practices.

Tutor Notes

- The above essay is pretty short and to the point and would pass. If you want to beef out the essay you can include some of the following information for a higher score:

- Stakeholders can be harmed by, or benefit from the organisation (can affect and be affected by the organisation). For example a stakeholder can be harmed if the organisation becomes involved in illegal or immoral practices- e.g. the local community can suffer if the organisation begins to pollute the local rivers. The local community can also benefit from the organisation through increased employment levels.

- CSR argues organisations should respect the rights of stakeholder groups

- Stakeholders are important because they may have direct or indirect influence on decisions

- The public sector has a wider and more complex range of stakeholders as they're managed on behalf of society as a whole. They're more likely to take a rage of stakeholder views into account when making decisions. However, these stakeholders are less powerful - i.e. they can't threaten market sanctions, to withdraw funding, or to quit the business etc.

- The essay doesn't specifically ask you to Map Stakeholders, but you could throw in a cheeky mention of Mendelow's Stakeholder Matrix, perhaps in the conclusion. Don't spend time describing it though- you won't get more than 1 point for mentioning it. You'd be better off spending your time giving lots and lots of examples of different types of stakeholders.

- Study guide p. 58

NEW QUESTION # 22

Industry Sectors can be classified as Primary, Secondary and Tertiary. What is meant by an 'industry sector'?

Describe the main characteristics of and types of business you will find in these. (25 marks)

Answer:

Explanation:

See the solution in Explanation part below.

Explanation:

How to approach this question

- The first question can be a simple introduction with a bit of extra detail. The main 'meat' to your essay is going to be explaining the three sectors, their characteristics and example businesses.

- Aim for three well explained characteristics as a minimum

Example essay

An industry sector refers to a broad category or grouping of businesses and economic activities that share similar characteristics and functions in the production and distribution of goods and services. These sectors are often classified into three main categories: Primary, Secondary, and Tertiary. Here are the main characteristics and types of businesses you will find in each of these industry sectors:

1.Primary Sector:

*Characteristics: The primary sector involves activities related to the extraction and production of raw materials and natural resources directly from the environment. This sector relies on nature and weather patterns: businesses in the primary sector are highly dependent on natural factors such as climate, weather, soil quality, and geographic location. These factors can significantly impact the productivity and profitability of primary sector activities. Extreme weather such as floods can severely impact this sector. Moreover there is a seasonality to this sector and many activities in the primary sector require a significant amount of manual labour, particularly in agriculture, fishing, and forestry. However, modern technology has also been integrated into some primary sector activities to increase efficiency.

*Types of Businesses: a. Agriculture: This includes farming, crop cultivation, livestock raising, and forestry.

b. Mining and Extraction. c. Fishing and Aquaculture: Forestry and Logging: Includes the harvesting of timber and related activities.

2.Secondary Sector:

*Characteristic: The secondary sector focuses on the transformation of raw materials and intermediate goods into finished products. The main characteristic of the sector is that it requires high levels of machinery and industrial techniques. There is a reliance on technology. Secondly, the secondary sector adds significant value to the products compared to their raw material form. This value addition is achieved through processing, assembly, and quality control processes. The third main characteristic is standardisation: Manufacturing processes often involve standardization of components and processes to ensure consistency and quality in the final products. Standardization helps in economies of scale.

*Types of Businesses: a. Manufacturing: This sector includes factories and plants that produce tangible goods such as automobiles, electronics, textiles, and machinery. b. Construction: Involves the building and construction of structures like buildings, bridges, and infrastructure. c. Utilities: Companies providing essential services like electricity, gas, and water supply fall into this category.

3.Tertiary Sector:

*Characteristic: The tertiary sector is also known as the service sector and involves businesses that offer various services to consumers and other businesses. The main defining characteristic of this sector is Intangibility: Services are intangible and cannot be touched or held. They are often experienced directly by consumers through interactions with service providers or through the use of technology. Secondly, High Human Involvement: The tertiary sector relies heavily on a skilled and often highly educated workforce to deliver services effectively. This can include professionals such as doctors, lawyers, teachers, and customer service representatives. Lastly, Customization: Many services are customized to meet the specific needs and preferences of individual clients or customers. This personalization is a key characteristic of the tertiary sector. For example Legal Advice will always be different depending on the specific needs of the client.

*Types of Businesses: a. Retail and Wholesale: Businesses engaged in the sale of goods to consumers or to other businesses. b. Healthcare and Education: This includes hospitals, clinics, schools, colleges, and universities. c. Financial Services: Banks, insurance companies, and investment firms are part of this sector. d.

Hospitality and Tourism: Hotels, restaurants, travel agencies, and entertainment venues fall into this category.

e. Professional Services: Legal, accounting, consulting, and IT services are part of the tertiary sector.

These industry sectors represent the different stages of economic activity, with the primary sector providing raw materials, the secondary sector processing and manufacturinggoods, and the tertiary sector offering services and distribution. Together, these sectors form the backbone of an economy, contributing to its growth and development Tutor Notes

- I've gone overboard on naming the types of organisation in the different sectors. You don't have to remember all of these. 3 examples is sufficient to get good marks. I've just named them all so you can see what could be considered a right answer.

- Some people are talking about Quaternary and Quinary Sectors. CIPS is not one of those people, so don't worry if you come across those terms in any further reading. But FYI

1.

*Quaternary Sector: This sector involves knowledge-based activities, including research and development, information technology, and data analysis.

*Quinary Sector: The quinary sector comprises high-level decision-making and leadership roles in areas such as government, academia, healthcare, and top-level corporate management.

- LO 4.1 p.196

NEW QUESTION # 23

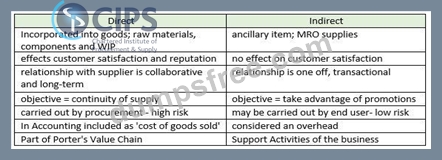

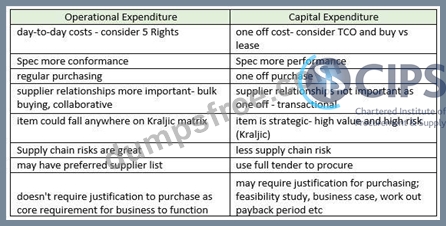

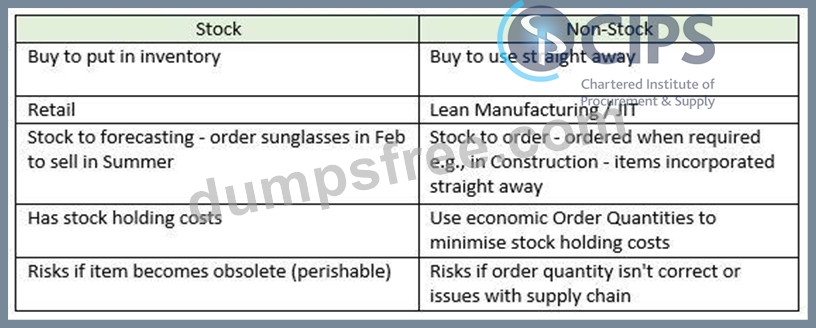

Explain, with examples, the three different ways one can categorise procurement spend: direct vs indirect, capital expenditure vs operational expenditure and stock vs non-stock items. (25 points)

Answer:

Explanation:

See the solution in Explanation part below.

Explanation:

The knowledge to remember:

A table with text on it Description automatically generated

Essay Plan :

Remember to include examples for each of the six categories of spend. This is specifically asked for in the question so it's important to include as many examples as you can. To do this you could take an example organisation such as a cake manufacturer and explain which of their purchases would fall into each category and why.

Introduction - explain why procurement categorises spend

- Direct - these are items that are incorporated into the final goods (the cakes) so would include raw materials such as flour, eggs, sugar etc

- Indirect - these are items that the company needs, but don't go into the end product. For example, cleaning products and MRO supplies for the machines

- Capital Expenditure- these are large one-off purchases, such as buying a new piece of equipment such as a giant oven to cook the cakes.

- Operational Expenditure - these are purchases that are required to ensure the business can function day-to- day. They may include PPE for the workers in the factory and cleaning equipment

- Stock items - these are items procured in advance and held in inventory until they are needed. In a cake manufacturing factory this could be PPE for staff such as hairnets and gloves. The organisation will buy these in bulk and keep them in a stock cupboard, using these as and when they are required

- Non- stock items - items that are not stored and used right away. An example would be eggs- these will need to be put directly into the cakes as they would go off if bought in advance.

Conclusion - the categories are not mutually exclusive - an item can be direct and operational, or indirect and stock. Different companies may use different systems to classify items of spend.

Example Introduction and Conclusion

Introduction

Procurement categorizes spend to efficiently manage resources and make strategic decisions. Three primary ways of categorizing procurement spend include distinguishing between direct and indirect spend, classifying expenditures as capital or operational, and categorizing items as stock or non-stock. These distinctions aid organizations in optimizing their procurement strategies for better resource allocation.

Conclusion:

In conclusion, categorizing procurement spend into direct vs. indirect, capital vs. operational, and stock vs.

non-stock items is essential for strategic resource management. While these categories provide a structured framework, they are not mutually exclusive, as an item can fall into multiple categories. For example, an item may be both direct and operational or indirect and stock. The flexibility of these categories allows organizations to tailor their procurement strategies based on their specific needs, ensuring efficient resource allocation and effective supply chain management. Different companies may adopt varying categorization approaches depending on their industry, size, and operational requirements.

Tutor notes:

- Because you've got 6 categories of spend to talk about you're only going to need 3-4 sentences for each.

Providing you've said the category, explained what it is and given one example, you'll absolutely fly through this type of question

- You could also mention that it is useful to use categories of spend as this helps with budgeting. Different categories may also have different processes to follow for procuring the item (this could form part of your introduction or conclusion).

- This subject is LO 1.3.2 it's quite spread out in the text book but the main info is on p.49

- Note- different companies/ industries classify items of spend differently. Particularly packaging and salaries.

Some say they're direct costs and some say they're indirect costs. Honestly, it's a hotly debated subject and I don't think there is a right or wrong. I'd just avoid those two examples if you can and stick to ones that aren't as contentious like eggs and PPE.

NEW QUESTION # 24

Explain what is meant by added value (5 points). Describe 4 ways the Procurement Department can add value for their organisation (20 points)

Answer:

Explanation:

See the solution in Explanation part below

Explanation:

What to include in the essay:

- Definition of added value: the economic enhancement given to products or services before offering them to customers. Examples may include a product which has additional features at no additional cost to the customer or the provision of an extended warrantee.

- Description of four of the following with examples and s: providing better customer service levels, risk management, cost control and reduction, relationship management, reputation management, innovation, use of technology, streamlining processes, improving specifications, increasing sustainability, improving quality, ordering processes such as bulk ordering, inventory management, improving the product from the customer's perspective (e.g. packaging, exclusivity), sustainability, convenience, market development.

Example essay:

Added value in procurement refers to the enhancement or improvement in the economic worth, quality, or utility of products or services before they are offered to customers or end-users. In the context of procurement, the goal is to go beyond simply obtaining goods or services at the lowest cost. Instead, procurement aims to contribute additional value to the organization through various means. This essay explores the concept of added value and outlines four ways the Procurement Department can contribute to organizational improvement.

Improving Specifications

Procurement can add value firstly by ensuring all critical items are procured against a specification, and secondly by improving and regularly updating those specifications. For example, the procurement department might be responsible for procuring light-bulbs for an office. Having an effective specification for this purchase (lightbulbs must meet X safety standard and Y environmental standard) would result in less maverick buying for the organisation and the procurement of a better-quality product. Furthermore, regularly updating specifications ensures that purchases are made against current safety standards and regulations (e.g. the use of low-energy lightbulbs). If procurement don't update specifications, then there is a risk that items are bought that don't meet the correct standards. Added value in this regard could also therefore be considered the removal of risks of procuring the wrong item.

Stream-lining Processes

Procurement can add value by stream-lining processes such as requisitions and POs. This reduces the time it takes to procure an item, thus saving the company money. Another process that could be streamlined is the re-ordering process of regularly bought items. This could be automated when the stock levels reach a certain level. For example if an organisation requires its staff to wear PPE, an automatic request could be made once there are only 50 face masks left.

Managing Supplier Relationships

Having strong, positive relationships with suppliers is a source of added value as it means suppliers value you as a buyer and are therefore more likely to help in situations which are adversely affecting business. For example, if a manufacturer puts an order in for 300 items with their supplier but then realises that they have made an error in the amount, if there is a strong relationship, the supplier may allow the buyer to amend the order after the fact. If there is a poor relationship, the supplier may not be as flexible. The flexibility in the supply chain is therefore a source of added value.

Improving Quality / Innovation

This involves adding value from the customer's perspective. E.g. a customer may choose to purchase a phone that has a longer battery life than others. Procurement's role in this may be in completing a Value Engineering exercise or procuring higher quality components or materials at the same price in order to achieve this additional feature.

In conclusion, the Procurement Department plays a crucial role in organizational success by adding value through improved specifications, streamlined processes, strong supplier relationships, and a focus on quality and innovation. These strategies contribute to enhanced efficiency, reduced risks, and increased customer satisfaction, making procurement an essential function for organizational excellence.

Tutor Notes

- The question asks specifically to name 4 ways of adding value. You therefore won't get any additional points if you talk about 5 or 6, even though it may be tempting. Instead, focus your response on providing more information on the 4 you have chosen and bulking out your answer with examples. This demonstrates to the examiner that you fully understand the topic AND that you can apply the theory to real situations.

- You could use real-life examples from your own organisation/ experience or you could give a hypothetical situation such as a cake manufacturer. You could talk through how the procurement department at the cake manufacturer can add value by doing the four things in your essay: by amending the specification so the cakes are more tasty, by streamlining the process for ordering flour, by managing the relationship with the company that fixes the machines when they break down, and by introducing innovation such as using an e-procurement system to source raw materials and the benefits that these will bring to the organisation.

- Added value is part of the copyright for Learning Outcome 1.2 starting from p.19 but I'm gonna be honest, I think the new study guide is a bit crap on this part of the copyright. The section starts talking about the 5 rights of procurement and I think that makes things very confusing for students. The 5 rights and added value are linked subjects, but they're not the same. Getting the rights right, CAN lead to sources of added value, but added value is value that is IN ADDITION to what is expected. So, when you have a question on added value, focus on stuff that's listed under 1.1.4 'other sources of added value' on p.35 rather than talking about the 5 rights of procurement. My list at the top is more exhaustive than the one in the study guide.

- If you're looking to be really clever you can quote Michael Porter on 'what is added value?'. Michael Porter looks at this from a customer perspective - 'added value' refers to the addition of greater value (either by reducing the cost to produce it, or by adding something that customers are willing to pay more for). These could be; marketing / design, customer service, maintenance, delivery etc. This comes up at Level 5 / 6.

NEW QUESTION # 25

......

Our CIPS L4M1 qualification test help improve your technical skills and more importantly, helping you build up confidence to fight for a bright future in tough working environment. Our professional experts devote plenty of time and energy to developing the L4M1 Study Tool. You can trust us and let us be your honest cooperator in your future development. Here are several advantages about our CIPS L4M1 exam for your reference.

L4M1 Valid Exam Sims: https://www.dumpsfree.com/L4M1-valid-exam.html

- Free PDF Quiz 2026 CIPS L4M1: Scope and Influence of Procurement and Supply – High Pass-Rate New Test Tutorial ???? Simply search for 【 L4M1 】 for free download on [ www.validtorrent.com ] ????L4M1 Test Dumps Free

- Exam L4M1 Reference ???? L4M1 Updated CBT ⏬ Exam L4M1 Testking ???? 《 www.pdfvce.com 》 is best website to obtain ⮆ L4M1 ⮄ for free download ????L4M1 Updated CBT

- Test L4M1 Dates ???? Exam L4M1 Flashcards ???? L4M1 Test Dumps Free ???? Search for ⇛ L4M1 ⇚ and obtain a free download on ( www.practicevce.com ) ????Valid L4M1 Test Guide

- L4M1 Updated CBT ♻ Exam L4M1 Flashcards ???? L4M1 Valid Exam Forum ???? Search for ➡ L4M1 ️⬅️ and easily obtain a free download on ➤ www.pdfvce.com ⮘ ????Official L4M1 Study Guide

- Free PDF Quiz 2026 L4M1: Fantastic New Scope and Influence of Procurement and Supply Test Tutorial ???? The page for free download of ➤ L4M1 ⮘ on ➠ www.dumpsmaterials.com ???? will open immediately ????Exam L4M1 Testking

- L4M1 New APP Simulations ???? L4M1 Valid Exam Forum ???? Exam L4M1 Flashcards ???? Search for ▛ L4M1 ▟ on ➽ www.pdfvce.com ???? immediately to obtain a free download ????L4M1 Test Dumps Free

- Latest L4M1 Test Sample ✨ Latest L4M1 Test Sample ⬅️ Test L4M1 Book ???? Search for 《 L4M1 》 and easily obtain a free download on ➡ www.pdfdumps.com ️⬅️ ????Test L4M1 Book

- L4M1 pdf copyright, CIPS L4M1 real copyright, L4M1 valid dumps ???? “ www.pdfvce.com ” is best website to obtain ➠ L4M1 ???? for free download ????L4M1 Updated CBT

- Free PDF Quiz 2026 L4M1: Fantastic New Scope and Influence of Procurement and Supply Test Tutorial ⚪ Enter ▶ www.prep4away.com ◀ and search for 「 L4M1 」 to download for free ????L4M1 Test Duration

- 100% Pass Quiz 2026 Professional L4M1: New Scope and Influence of Procurement and Supply Test Tutorial ???? Download ▷ L4M1 ◁ for free by simply searching on ⏩ www.pdfvce.com ⏪ ????Exam L4M1 Testking

- 100% Pass Reliable L4M1 - New Scope and Influence of Procurement and Supply Test Tutorial ???? Copy URL ➡ www.pdfdumps.com ️⬅️ open and search for ⏩ L4M1 ⏪ to download for free ????Latest L4M1 Test Sample

- directoryark.com, lucmhcg702643.59bloggers.com, baidubookmark.com, bookmarkvids.com, flynnxjts021936.vigilwiki.com, francespjxa324562.blog2freedom.com, bookmarkinglog.com, darrenhfnz882775.liberty-blog.com, bookmarksusa.com, oisifjzz606031.mysticwiki.com, Disposable vapes

P.S. Free 2026 CIPS L4M1 dumps are available on Google Drive shared by DumpsFree: https://drive.google.com/open?id=1yJDlB9sje6TAVMiDNezhIrjTqSv8F0tO

Report this wiki page